Revisiting Association Health Plans

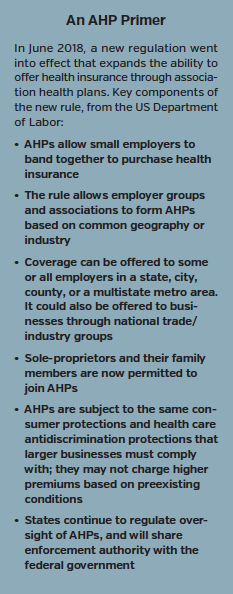

In early 2018 the US Department of Labor proposed a rule that would alter the regulation of association health plans (AHPs). The proposal came on the heels of an executive order by President Trump to allow more employers to form AHPs. The regulation was finalized in June. Since then, 28 new AHPs have popped up in different states (See sidebar).

First Report Managed Care first analyzed association heath plans in its February 2018 issue. Now revisiting the topic, we have consulted our panel of experts. Specifically, a year later are they seeing any telling trends? Were concerns about potential negative impact AHPs would have on the ACA overblown? What about the checkered past of AHPs and potential defrauding? Where are commercial payers fitting in? Our panelists include:

- Melissa Andel, vice president of health policy, Applied Policy, Washington, DC

- Larry Hsu, MD, medical director, Hawaii Medical Service Association, Honolulu.

- Daniel Sontupe, executive vice president and director market access & payer marketing, The Bloc Value Builders, New York

- F. Randy Vogenberg, PhD, RPh, principal, Institute for Integrated Healthcare, Greenville, SC

When we last visited this issue, some expressed concern that AHPs would bring about negative selection, leaving mostly sicker individuals in the ACA plans. Others thought that such plans addressed only a narrow slice of the market so the impact would be minimal. Do we know at this early stage which is true?

Mr Sontupe: I believe the jury is still out on how broader risk pools might be impacted. We are seeing plans develop in 13 states, but we have no real data on how these plans are working out. They are for the most part fully-insured plans, giving even more power to those commercial payers.

At this point it looks as if the so-called healthy-person plan is not arising. However, I am skeptical about savings attributed to these plans and will be surprised if the premiums stay as low as they currently are.

Ms Andel: It is still too early to see how the broader risk pool will be impacted by AHPs. The plans aren’t even a year old yet. Another problem is that the introduction of AHPs coincided with the repeal of the individual mandate. That might make post hoc analysis challenging because it will be difficult to sort out people who left the exchange pool for AHPs from people who left the exchange pool because the individual mandate is no longer in effect.

Dr Hsu: There still is a lot of work to be done to promote a broad acceptance of these plans. The risk pool needs to represent not only the sick or healthy, but all patients.

Dr Vogenberg: I agree that it is too early to tell and there are too many variables. Still, AHPs continue to look promising.

A year ago, there was concern about the potential to defraud unwitting customers. The Trump administration acknowledged that in the past some AHPs have “failed to pay promised health benefits to sick and injured workers while diverting…employer and employee contributions from their intended purpose.” It has installed safeguards designed to prevent defrauding. Are the precautions working, or is this another area where it is too soon to tell?

Mr Sontupe: It looks as if some of the safeguards are working. For example, the [provisions for] regional plans to ensure they support like-minded individuals acting in unison. This works as a protection against fraud.

Dr Hsu: I agree. But more work still needs to be done to ensure that the safeguards are being managed and up to date to prevent future problems. There has to be ongoing oversight and management.

Dr Vogenberg: I would point out that the Department of Labor needs to avoid being too heavy handed. The market is not dumb or unregulated, nor are those involved foolish.

Ms Andel: It is too early to draw any hard conclusions. One thing I found interesting from looking at the data is that chambers of commerce are the most common AHP sponsor and that about half of AHP plans offer health savings accounts. That tells me that they may be attractive to high-earning small business owners. That customer base may be more knowledgeable about the insurance industry, perhaps because they have been in the individual market for a while.

Proponents are pointing to the farm cooperative Land O’Lakes plan as an example of success. It is offering insurance to farmers in Nebraska and Minnesota. Premiums are reportedly expected to be at least 25% less than what these farmers can get on the ACA marketplace in Nebraska, and 10% less than in Minnesota. What does that tell you?

Mr Sontupe: We need to keep an eye on initial premiums. Too often, premiums are launched steep discounts until insurance companies realize they are not making enough money. Then premiums go up aggressively. That was an issue with ACA exchange plans early on. The other concern will be the removal of benefits while keeping premiums the same. These are areas that the buyers and associations need to be aware of.

Ms Andel: Here, too, I think it is too early to tell. One question about AHPs was whether they would be able to offer an attractive benefit package at a competitive price, especially since the benefits that consumers want are also the benefits that drive up premiums. It looks like they have been able to do that, at least initially.

But, as Mr Sontupe noted, we had a similar experience in 2014, where exchange plans underpriced premiums and then had to increase premiums in years 2, 3, and 4 to make up for that. Maybe the actuaries were able to price these correctly, but we won’t know until we have a full year of medical claims data.

I would also add that Nebraska is also a bit of an outlier because it is one of the states where the exchange is really struggling. Experiences in other states may vary. In other words, Nebraska may be a perfect storm for AHPs, and maybe that is where they will find their niche: As a good option in certain markets.

Dr Hsu: I agree that it is hard to extrapolate what is happening in a single region to the general marketplace. Only time and experience will tell whether or not this is an exception.

Dr. Vogenberg: Just as we saw issues with ACA era physician group practice initiatives around taking risk, it will take several years of experience to know what is or is not working with AHPs.

It is not surprising that self-insured AHPs are a rarity at this stage. The need for third-party sponsorship presents opportunities for commercial insurers. UnitedHealthcare and Blue Cross Blue Shield are leading the charge. What do you make of this opportunity?

Mr Sontupe: I absolutely expected insurance companies to get involved and go big. To be self-insured would be very difficult for these associations. There is quite a bit of analysis involved that a number of associations may not be prepared for. It makes sense to push out the risk have a predictable premium payment offered to all members.

Dr Vogenberg: I agree. Depending on experience, book of current business, and fiscal stability, any insurance firm holding risk or any third-party administrator could offer or support AHPs in their area of interest geographically or industry type.

Dr Hsu: While most insurance companies are conservative and risk-averse, they also see opportunity. and want to be part of these potential solutions. They also need to remain competitive.

Is there anything to make of patterns that are developing? Does the fact that most AHPs are fully-insured, regional, and located primarily in the middle of the country and in the South tell you anything?

Mr Sontupe: The overall numbers at this point are still relatively small. I hold to the need to see more data as to how these plans work out in the long run.

Dr Vogenberg: There appears to be interest among small- to medium-size employers who wish to investigate all opportunities to better manage their health insurance risk.

The Trump administration has been given credit for its efforts to address rising prescription drug prices. Does it deserve recognition here too—especially since some thought that AHPs were a bad idea (for reasons mentioned earlier)?

Dr Vogenberg: AHPs fit a narrow need in the market and does represent a success by the Trump administration so far. The fact that traditional insurance carriers have jumped in shows there is value.

Mr Sontupe: I believe it is too early to give credit or point fingers. Let’s see how this plays out in year 2, and let’s see what happens when claims are being made through these plans. Today the data is about enrollment and premiums. We don’t yet know how things are going to actually play out.

Ms Andel: I think we need to go through a complete plan year before we declare anything a success, but it seems likely that some of the concern over AHPs were overstated.